Investment Lessons from the Bull Market Cycle and the Wall of Worry

- Summit Puri

- May 4

- 5 min read

More than three-and-a-half years have now passed since the bull market got underway in October 2022. At that time, inflation was climbing at its fastest rate in fifty years, the Fed was in the midst of hiking interest rates, and ChatGPT had yet to be released to the public. In the time since, the S&P 500 has more than doubled in value and the Bloomberg U.S. Aggregate Bond index has made a full recovery.

While the world looks considerably different today than it did then, one thing that has not changed is the presence of market-related concerns in the headlines. Every cycle introduces new challenges and prompts questions about whether the time-tested rules of investing still hold up. The reality is that each cycle is distinct, marked by its own catalysts, innovations, and sources of uncertainty. And yet, the core principles of investing and financial planning have remained consistent across decades, and have continued to guide investors in the right direction this year.

Bull markets climb a wall of worry

Even as geopolitical developments continue to influence markets, the more meaningful consideration for long-term investors may be the overall market cycle. With the market trading near all-time highs, it is natural for some investors to feel uneasy about the possibility of pullbacks and corrections. These events can happen with some regularity. Historically, the S&P 500 has experienced four or five pullbacks of 5% or worse each year, on average.

While such events are never welcome, long-term investing is shaped far more by patterns that play out over years and decades. This is one reason why overreacting to short-term market moves can be counterproductive, potentially leaving investors poorly positioned relative to their long-term financial goals.

There is a common saying among investors that the market climbs a "wall of worry" on a regular basis. Over the past several years, markets have navigated high inflation, a banking crisis in 2023, geopolitical conflicts, the risk of a Fed policy error, AI-related market concentration, tariff-driven volatility, and more. None of these challenges were insignificant, and yet, through all of them, the market has continued to perform well.

The chart above illustrates this pattern going back to World War II. Over this 70-year stretch, bull markets have lasted considerably longer and produced much larger gains than what is typically lost during bear markets. Bear markets have generally lasted one to two years on average, while recent bull markets have run as long as ten years or more. Even when corrections occur within bull markets, the average decline has been 14%, with the average recovery taking just four months.

Consider the bull market that followed the 2008 financial crisis, which lasted nearly eleven years. Despite this remarkable run, it is often called "the most unloved bull market" because there was a near-constant stream of market and economic concerns throughout. In hindsight, it is clear that even when those concerns were legitimate — such as worries about the pace of the economic recovery or the level of the national debt — they did not warrant changes to long-term portfolios.

Of course, past performance is no guarantee of future results, and how quickly markets recover depends on the specific circumstances involved. Still, the historical record clearly suggests that attempting to react to every market movement has, more often than not, caused investors to miss a significant portion of the gains that followed.

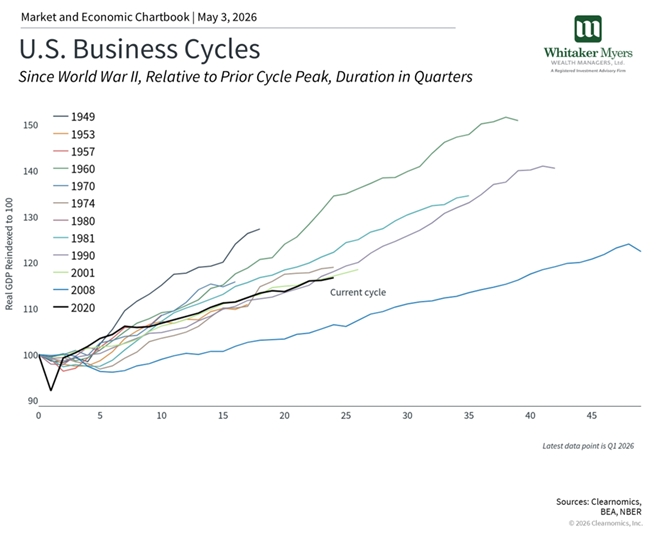

A growing economy is the foundation for long-run returns

While the stock market and the broader economy are not one and the same, they are closely connected. Corporate earnings are the primary driver of stock prices over the long run, and those earnings ultimately depend on economic growth. For this reason, it is important to keep a close eye on the broader economic cycle, even as markets respond to a wide variety of factors on a day-to-day basis.

The current business cycle has technically been running two-and-a-half years longer than the market cycle. The last official recession, as determined by the National Bureau of Economic Research, was the brief but sharp contraction caused by the pandemic in 2020. Since then, there have been quarters of slower growth and periodic forecasts of recession, none of which have materialized.

By many measures, the economy remains in good health today, though investors are closely monitoring three key areas of concern. First, oil prices above $100 per barrel, if sustained, could weigh on consumer spending and add to inflationary pressures. Second, the labor market has slowed noticeably, particularly in sectors such as technology, raising questions about consumer spending, which has been a key pillar of economic strength in recent years. Third, the scale of investment in AI has led some to question whether a "bubble" is forming — an understandable concern given that many of today’s investors lived through both the dot-com bust and the housing crisis.

Bubbles are notoriously difficult to identify in real time, and history shows that not every period of elevated valuations ends in a dramatic collapse. So far in this cycle, unlike in some prior periods, earnings growth has supported valuations and many companies are making substantial investments funded by their own profits. For long-term investors, the key is maintaining a balanced exposure across different parts of the market in order to participate in growth while managing risk.

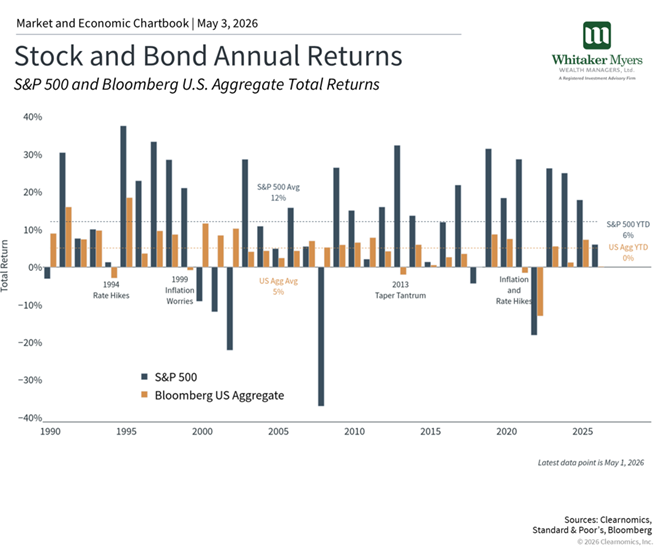

Stocks and bonds continue to complement each other

Every market cycle naturally prompts questions about whether traditional portfolio management principles still apply. In 2022, when both stocks and bonds declined at the same time due to rapidly rising inflation and interest rates, some investors questioned whether bonds still served a meaningful role in a diversified portfolio. Similar doubts emerged after the 2008 financial crisis, when bonds were challenged by historically low interest rates.

Over the past few years, bonds have not only recovered but have also provided meaningful income and portfolio stability. The Bloomberg U.S. Aggregate Bond Index delivered positive returns in each of the past two years, helping to offset periods of equity volatility. International stocks and commodities have also contributed, offering additional diversification benefits.

This pattern is consistent with what history has demonstrated across many cycles. Each period seems to spark the question of whether "this time is different" with respect to the relationship between asset classes. In the 1970s, inflation put pressure on traditional portfolios. During the dot-com era, technology stocks became enormously popular despite limited corporate profits, making other sectors appear unexciting by comparison. In 2022, rising interest rates created simultaneous headwinds for both stocks and bonds. Many of these challenges have echoes in the current environment.

Each time, a commitment to the principles of diversification and long-term investing has proven to be the right course of action. As uncertainty persists and new headlines continue to move markets, focusing on the broader picture remains as important as ever.

How does this impact you? Remember that more than three-and-a-half years into this bull market, the foundational principles of long-term investing remain as relevant as they have ever been. Markets have consistently rewarded investors who maintain balanced portfolios and remain focused on their long-term financial goals. If you’re unsure, need to review your goals, or are looking for a second opinion, connect with one of our financial advisors today. Our team is always ready and willing to help, with the heart of a teacher.